February 2026 Edition Vol. 1The Current State of the Japanese Real Estate Market Key Market Changes Foreign Investors and Prospective Migrants Should Watch This Month

Summary

When viewed from the perspective of foreign investors, the current state of Japan’s real estate market this month is relatively clear. The Japanese market continues to maintain its appeal as an investment destination, but it is no longer a phase in which any property can be purchased indiscriminately. Selection is increasingly shifting toward highly liquid urban assets and asset types that are more likely to benefit from supply constraints.

In particular, when looking at this month’s real estate price indices, REINS transaction data, construction cost indices, exchange rates, and foreigner-related policies together, several structural trends become apparent. Rising construction costs and restrained new housing supply are supporting the prices of existing properties, while the weaker yen is lowering the acquisition threshold for foreign buyers. At the same time, however, the practical operation of residence status and foreigner acceptance systems appears to be moving in a stricter direction.

In other words, this was a month in which easier purchasing conditions and more difficult institutional requirements advanced at the same time.

The Overall Shape of the Japanese Market

Asset Selection Is Advancing Amid a Rising Market

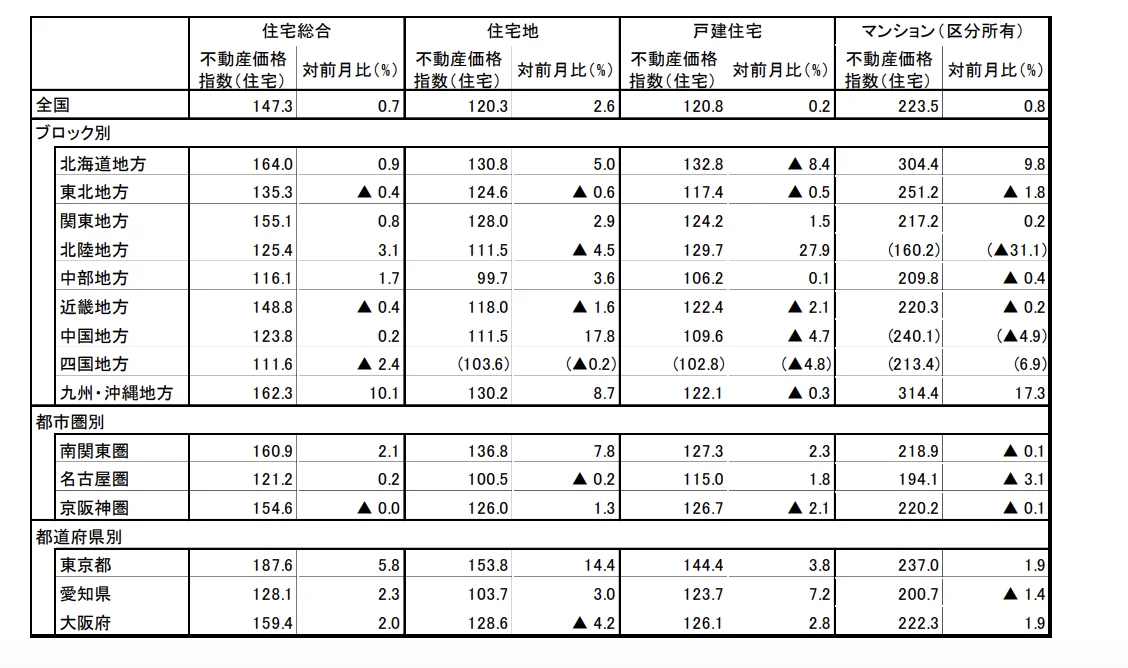

First, let us look at prices. According to the Real Estate Price Index published by Japan’s Ministry of Land, Infrastructure, Transport and Tourism, the overall residential property index stood at 147.3 as of November 2025, up 0.7% month-on-month. Using 2010 as the base year of 100, this means that Japanese residential property prices have risen to approximately 1.5 times their previous level.

However, what characterizes this month’s market is not simply the overall rise in residential property prices, but the clear strength of the condominium segment. The index for condominium units has reached 223.5, more than double its 2010 level. By contrast, the detached house index remains at 120.8, and the gap between the two continues to widen.

For foreign investors, the key point here is that Japan’s residential property market is not a single uniform market. Condominiums in major metropolitan areas, particularly Tokyo, remain strong, while detached houses and regional residential properties do not follow the same logic. Even when purchasing with migration or personal use in mind, urban condominiums with stronger asset value are expected to retain a relative advantage when future resale or conversion to rental use is considered.

The Core of the Residential Market

Urban Condominiums Are Driving Price Formation

Source: Ministry of Land, Infrastructure, Transport and Tourism, Japan

Japan’s residential property market continues to maintain an upward trend, but the center of this growth has clearly shifted toward urban condominiums. While Japan’s overall population is declining, population concentration in Tokyo and other major metropolitan areas continues, supporting solid housing demand in urban areas. In addition, the low interest rate environment and continued inflows of overseas investment capital are also contributing to the rise in urban condominium prices.

This trend becomes even clearer when viewed by region. Tokyo’s condominium index has reached 237.0, significantly above the national average, indicating that Japan’s real estate market has a highly concentrated structure centered on Tokyo. Although price increases can also be observed in regional cities, the pace is clearly slower than in the Tokyo metropolitan area, and the price gap between regions may continue to widen going forward.

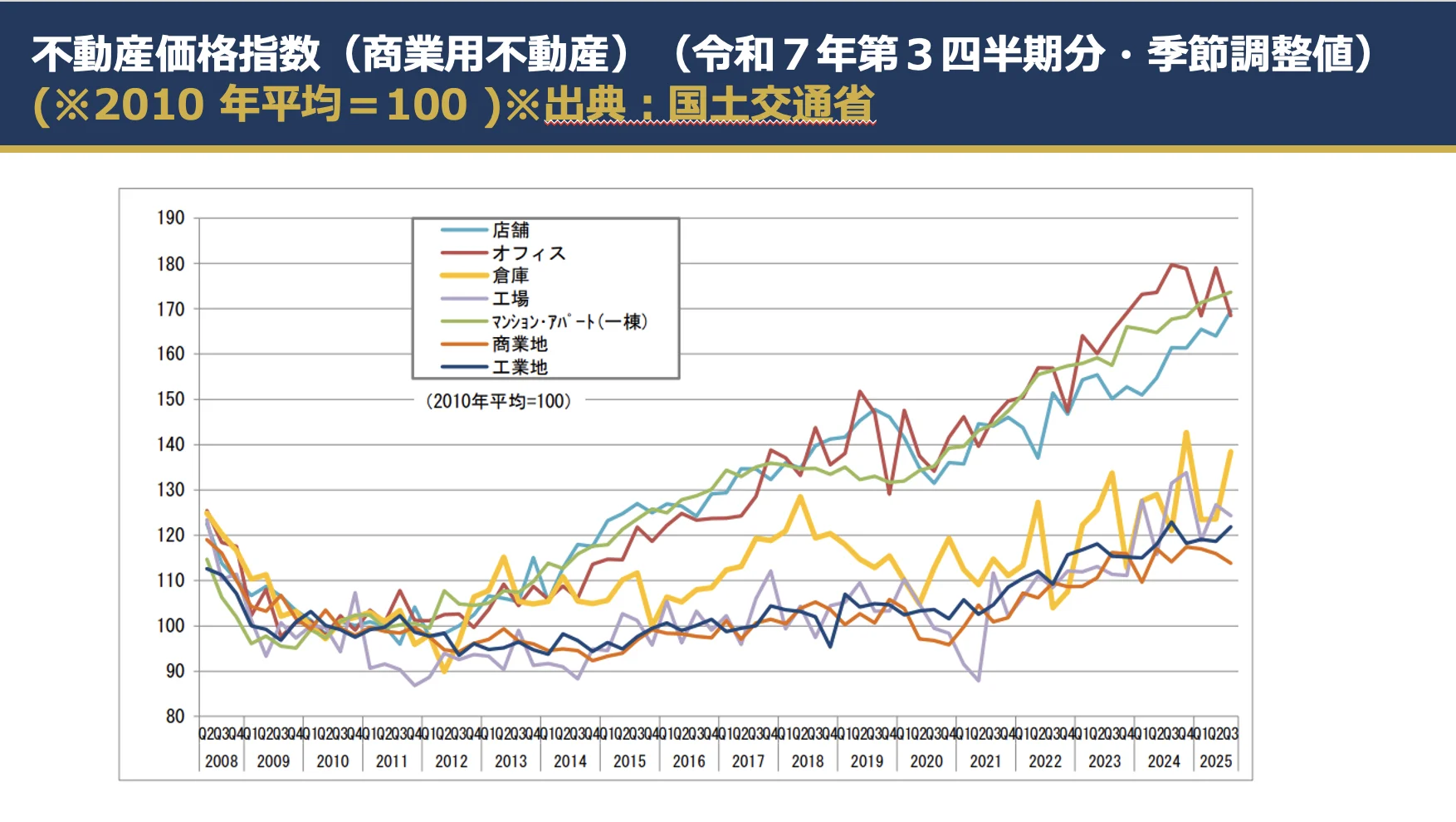

Selection Criteria for Income-Producing Real Estate

Market Disparities Emerging in Commercial Real Estate

The same logic applies to commercial real estate. The overall commercial real estate index stood at 147.2, up 1.1% quarter-on-quarter, showing a generally resilient trend. However, the stronger segments are not all commercial assets, but rather income-generating categories such as whole apartment buildings and retail properties. Office properties, by contrast, do not show the same clear upward momentum as residential assets.

For foreign investors, it is important not to view commercial real estate as a single broad category. Instead, assets need to be assessed by whether they can generate stable income and whether a clear exit strategy can be envisioned.

In Japan, properties with buildings that generate stable rental income have continued to receive higher market evaluations than vacant land with no income-producing capacity. In urban areas in particular, capital inflows into rental residential properties and retail-type assets remain ongoing, and no major change in this trend was observed this month.

On the other hand, in the office market, the spread of remote work and companies’ reassessment of office space requirements continue to have an impact, making asset-by-asset selection increasingly important.

Market Depth Indicated by Transaction Data

Asset Value Supported by Liquidity

Next, transaction data is particularly important. According to REINS-related statistics, as of December 2025, the number of newly listed properties remained on a downward trend, while the number of reported transactions continued to increase. Total listings, in other words inventory, also continued to decline. This indicates that, even amid insufficient supply in the market, properties with favorable conditions are still attracting buyers.

In the Greater Tokyo Area’s existing residential market, both transaction volume and prices for second-hand condominiums remained firm. Nationwide, the average transaction price for second-hand condominiums reached JPY 42.11 million, up 6.66% year-on-year, while the number of transactions also increased by 25.6%.

What this shows is that Japan’s market this month is not only experiencing price growth, but also an upward phase supported by liquidity. For foreign investors, ease of resale is more important than simply whether prices are high. In this sense, second-hand condominiums in urban areas with deeper transaction volume remain a strong candidate for consideration.

Price Support Viewed from the Supply Side

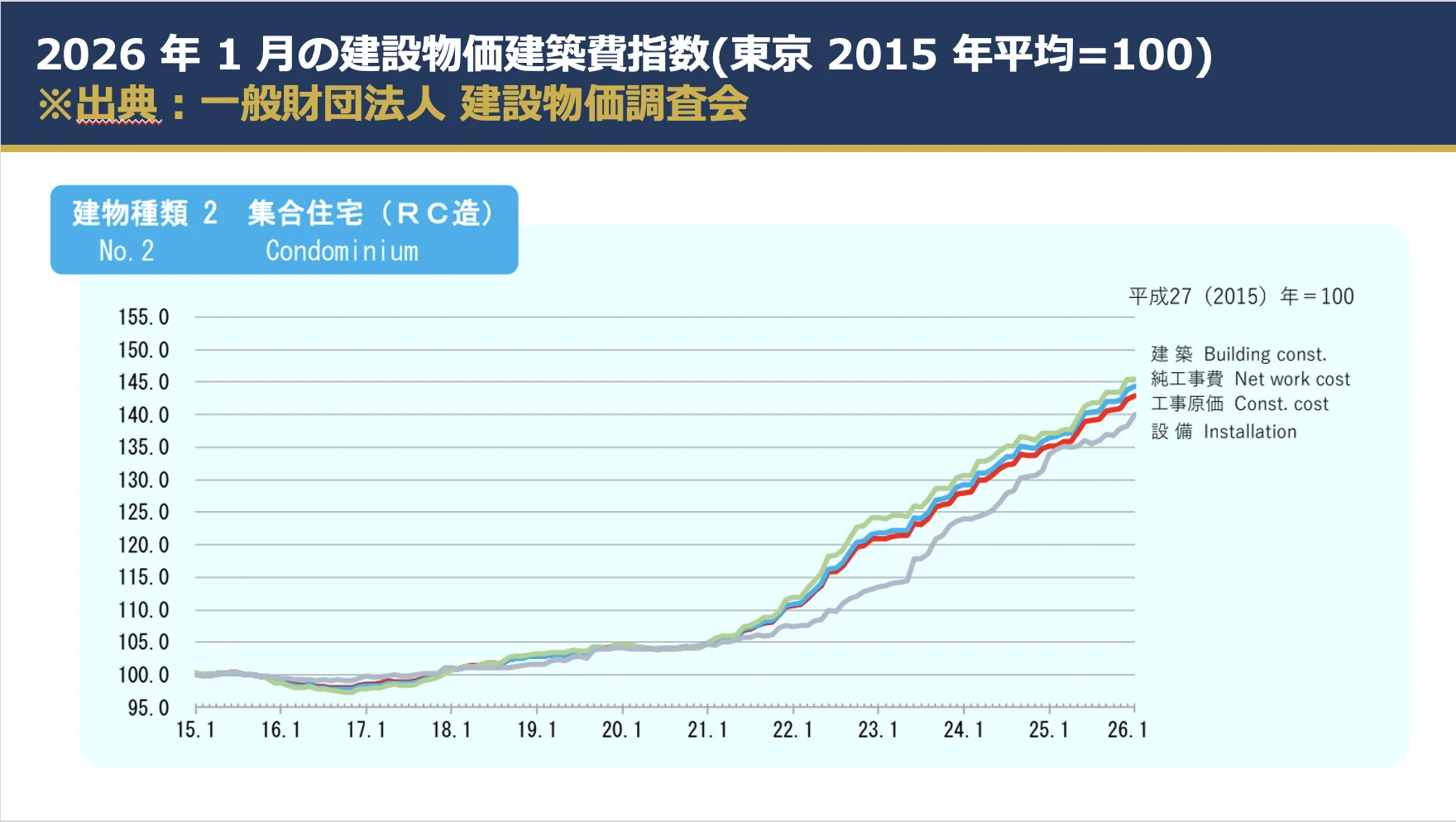

Rising Construction Costs and Constraints on New Housing Supply

What carries the greatest practical significance this month is the change in construction costs and the supply side of the market. According to the construction cost index, reinforced concrete apartment buildings reached 142.9 in January 2026, up 5.8% year-on-year. Compared with the base year, this represents an increase of approximately 43%. Based on a simple estimate, the construction cost per tsubo for RC condominiums is presumed to have risen to around JPY 1.43 million.

This is likely to push up the break-even point for development projects and place downward pressure on new housing supply.

Housing start statistics also show a decline in new housing starts, with rental housing, owner-occupied housing, and for-sale housing all showing weakness. In particular, the slowdown in the supply of newly built condominiums is likely to continue supporting prices for existing second-hand condominiums.

For foreign investors, the implication is clear. In an environment where new buildings are becoming more expensive and supply is difficult to bring to market, capital is more likely to flow into existing residential properties with high liquidity. This month can be described as one in which that structure became even more apparent.

Exchange Rate Environment and Investment Opportunities

Acquisition Timing Created by the Weaker Yen

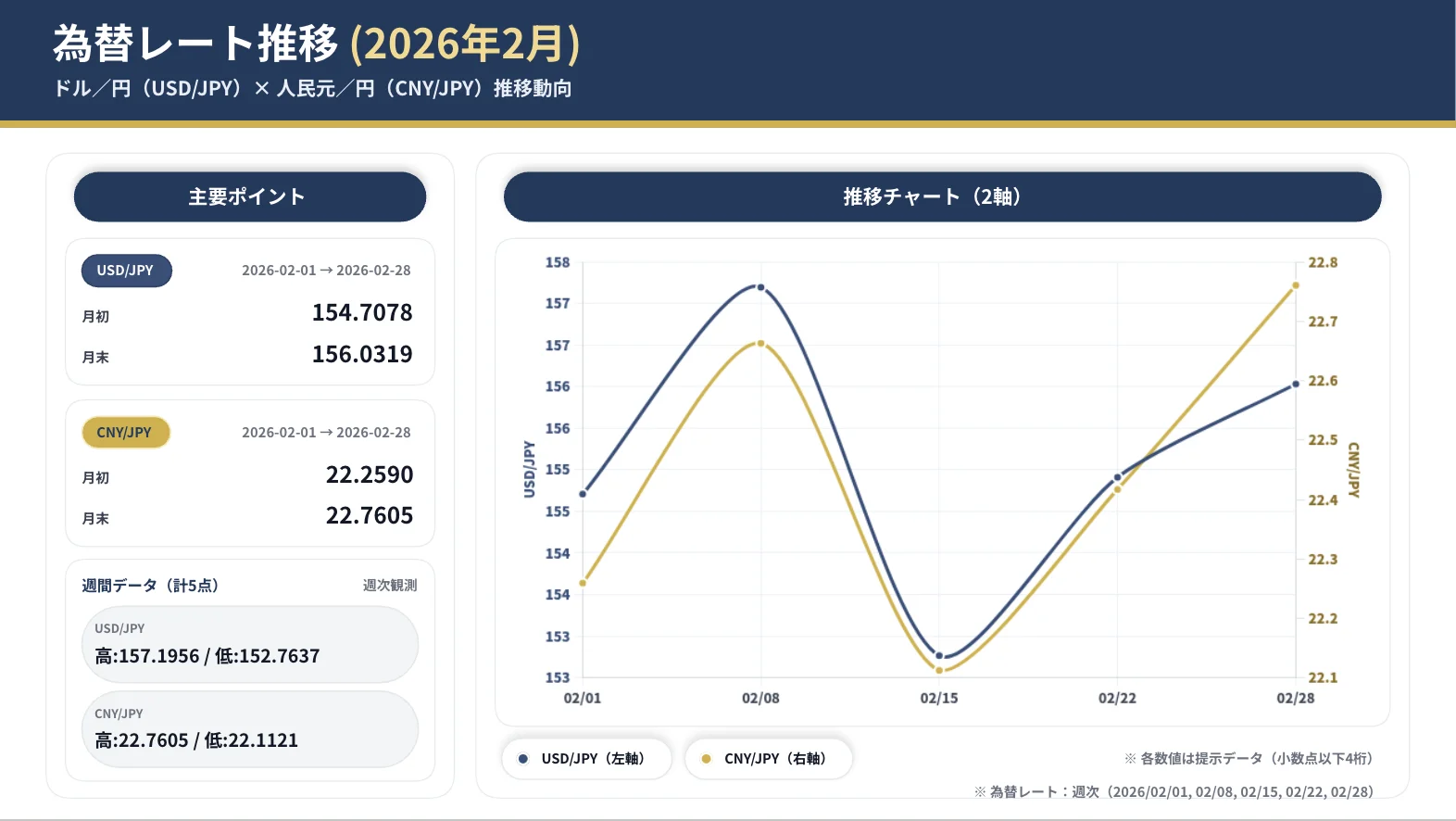

Exchange rates should not be overlooked. As of March 2026, the USD/JPY exchange rate is in the 158 yen range, while the JPY/CNY rate is around 0.0434 yuan per yen, indicating that the yen has weakened compared with one year earlier. For investors from China, Hong Kong, Taiwan, Singapore, and other markets, Japanese real estate has effectively become easier to acquire in local currency terms.

For example, even for a property priced at JPY 100 million, the amount of capital required is lighter than it was a year ago when viewed purely from an exchange rate perspective. This is likely to support capital inflows into condominiums, hotels, private lodging properties, and commercial real estate in Tokyo and Osaka.

That said, there are also points to keep in mind. A weaker yen is a tailwind at the time of purchase, but if the yen strengthens in the future, the actual return at the time of capital recovery may be compressed. Therefore, investment decisions this month should not be based solely on exchange rate advantages. It is important to confirm whether both rental income and resale liquidity can be secured.

Foreign Demand and a Turning Point in Policy

Institutional Refinement Advancing Behind Expanding Demand

From the perspective of foreign demand, both policy developments and statistical data confirm continued tailwinds for the market. According to JNTO, the number of foreign visitors to Japan in January 2026 was 3,597,500. Although this represents a year-on-year decline, the main reason was the seasonal effect caused by the timing shift of the Lunar New Year holidays.

In practice, demand from South Korea, Taiwan, Southeast Asia, Europe, and the United States remains strong, while Japan’s inbound demand is gradually becoming more diversified and less dependent on China alone. This is a positive factor for hotels, private lodging, and commercial facilities located around tourist destinations.

In addition, the number of foreign workers in Japan, as announced by the Ministry of Health, Labour and Welfare, has exceeded 2.57 million, reaching a record high. This is expected to support demand for rental housing, employee housing, and lifestyle-related commercial facilities. For readers considering migration, it is also clear that Japan continues to be a country that absorbs foreign demand.

However, from an institutional perspective, this month did not bring only reassuring signals. The Comprehensive Measures for the Acceptance of Foreign Nationals and Orderly Coexistence, decided on January 23, clearly indicated a direction of strengthening management while expanding acceptance. Measures such as digital transformation in residence management, stricter operation of residence status screening, and the introduction of JESTA suggest that Japan is not moving toward simple openness, but rather toward a more selective form of acceptance.

Furthermore, in relation to the Business Manager visa and permanent residency practices, there is a growing emphasis on business substance, employment structure, tax payment, and fulfillment of public obligations. The idea that buying real estate will make migration easier, or that establishing a company will naturally make it easier to obtain residence status, is risky.

For those considering migration or business operation in Japan, what needs to be designed is not only the real estate itself, but an integrated plan that includes visa strategy, employment, accounting, taxation, and actual residence status.

Which Assets to Select and Where Caution Is Required

As of this month, which assets appear promising?

First, highly liquid second-hand condominiums centered on Tokyo’s 23 wards. Prices are high, but the buyer base is deep, conversion to rental use is relatively easy, and exit strategies are easier to envision.

Second, lodging and commercial real estate in Osaka and major tourist destinations. These assets are more likely to benefit from the weaker yen and the diversification of inbound demand. However, properties that lack sufficient operational capability should be approached with caution.

Third, income-producing real estate in urban areas that can capture residential demand from foreign nationals.

On the other hand, assets that require caution include residential properties in regional areas with limited liquidity, special-purpose properties with restricted uses, and assets that carry heavy management burdens. Even if the headline yield appears high, investment efficiency may decline significantly if future resale buyers are limited.

This month’s market requires investors to focus not only on where to buy, but also on whether they can clearly identify who the asset can be sold to in the future.

Japanese Real Estate Investment Has Entered an Era of Selection

Overall, this month’s Japanese real estate market can be summarized as one that remains attractive to foreign investors, while selection and institutional preparedness have become increasingly important.

There is still value in buying, but not every location or property type is suitable. Japan continues to offer strong residential value, but property ownership and residence status are separate matters. The country also remains attractive as a base for business management, but only on the premise of substantive and sustainable business operations.

Above all, selecting assets that will be easier to sell in the future has become increasingly important in this month’s investment decision-making. This is not a phase for broad, indiscriminate purchasing. Rather, it is a market that requires careful selection based on four key factors: urban liquidity, supply constraints caused by rising construction costs, the benefits of the weaker yen, and the tightening of institutional requirements.

Contact Us

Thank you very much for reading this regular real estate column to the end once again.

If you are considering purchasing, selling, or managing real estate in Japan, please feel free to contact X&key Investment Partners Inc. We are able to provide support in Japanese, English, and Chinese.

Whether your purpose is migration, business management, personal use, or investment, we provide comprehensive advice and support from a practical perspective, taking into account your individual objectives, circumstances, investment goals, and exit strategy.